Taking advantage of new standards by the PCAOB and SEC, CFA Institute has been able to determine the composition of lead auditors for the S&P 500 including by gender and tenure.

Over the last decade, investors told audit regulators in the United States they wanted to know more about those involved in the audit of the companies in which they invest. Two recent changes have addressed that: the Audit Participants Standard (released by the SEC) and the New Audit Reporting Standard (released by the Public Company Accounting Oversight Board (PCAOB)). The requirements commenced in early 2017, but a full complement of data was not available until the filing of 2017 annual reports in early 2018.

Investors can now not only identify the audit firm issuing the opinion, but also the partner assigned to the engagement and to what degree other auditors were used by the primary auditor in reaching its conclusion on the financial statements. This information is now available to investors on the PCAOB’s AuditorSearch database by company name or ticker symbol. Investor can also determine by firm the auditor tenures.

For this exclusive report, CFA Institute identified the names of the lead engagement partners of companies comprising the Standard & Poor’s 500 Index (S&P 500). We used CalcBench to source the audit tenure of these same S&P 500 companies. We supplemented this data with manual verification. Because audit tenure was not required for all companies with a year-end prior to 15 December 2017, only 409 of the S&P 500 companies had provided such information as of the writing of this report.

Among our observations from review of the data are the following:

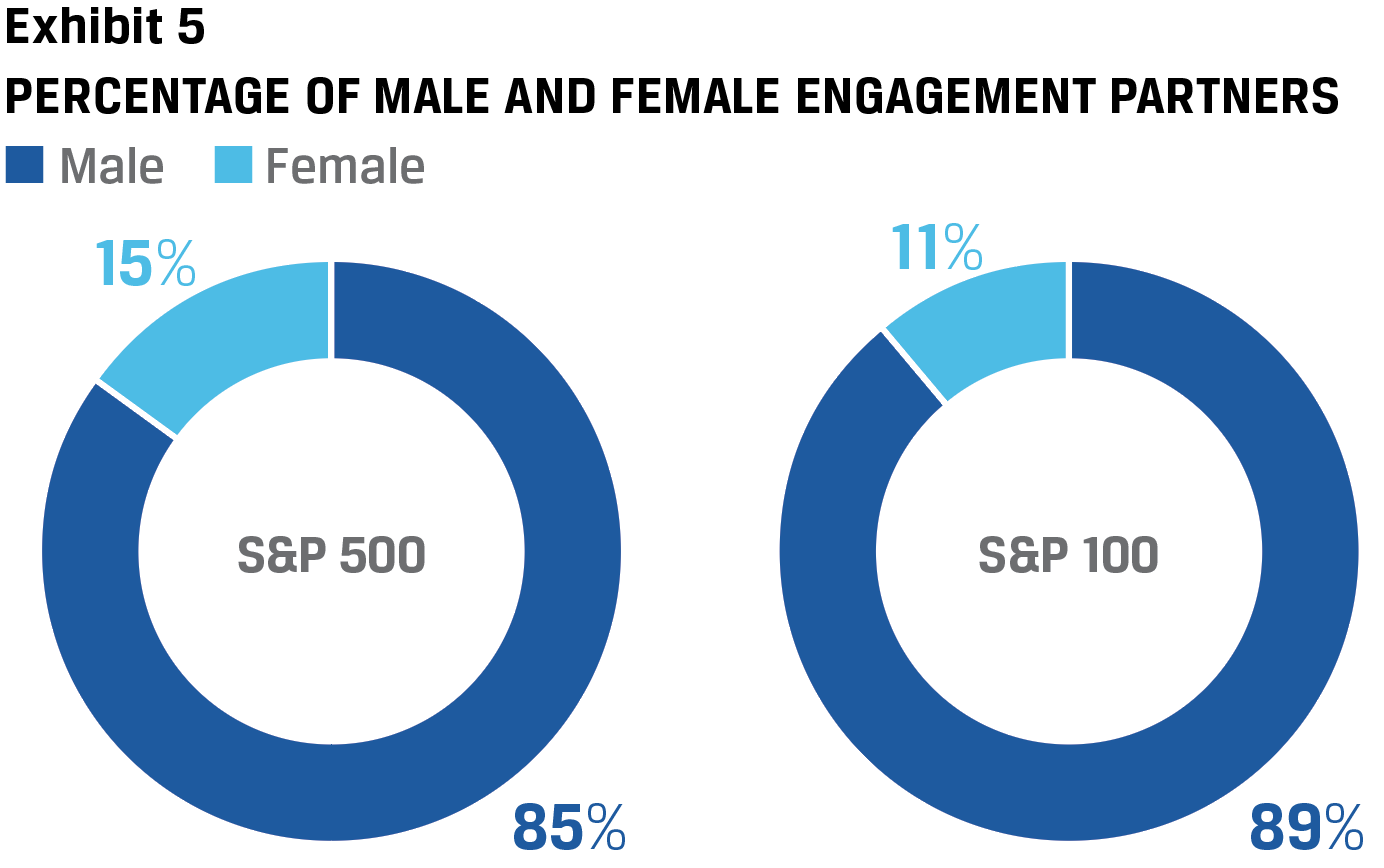

- Only 15% of lead engagement partners of the S&P 500 were female

- Only 11% of lead engagement partners of the S&P 100 were female

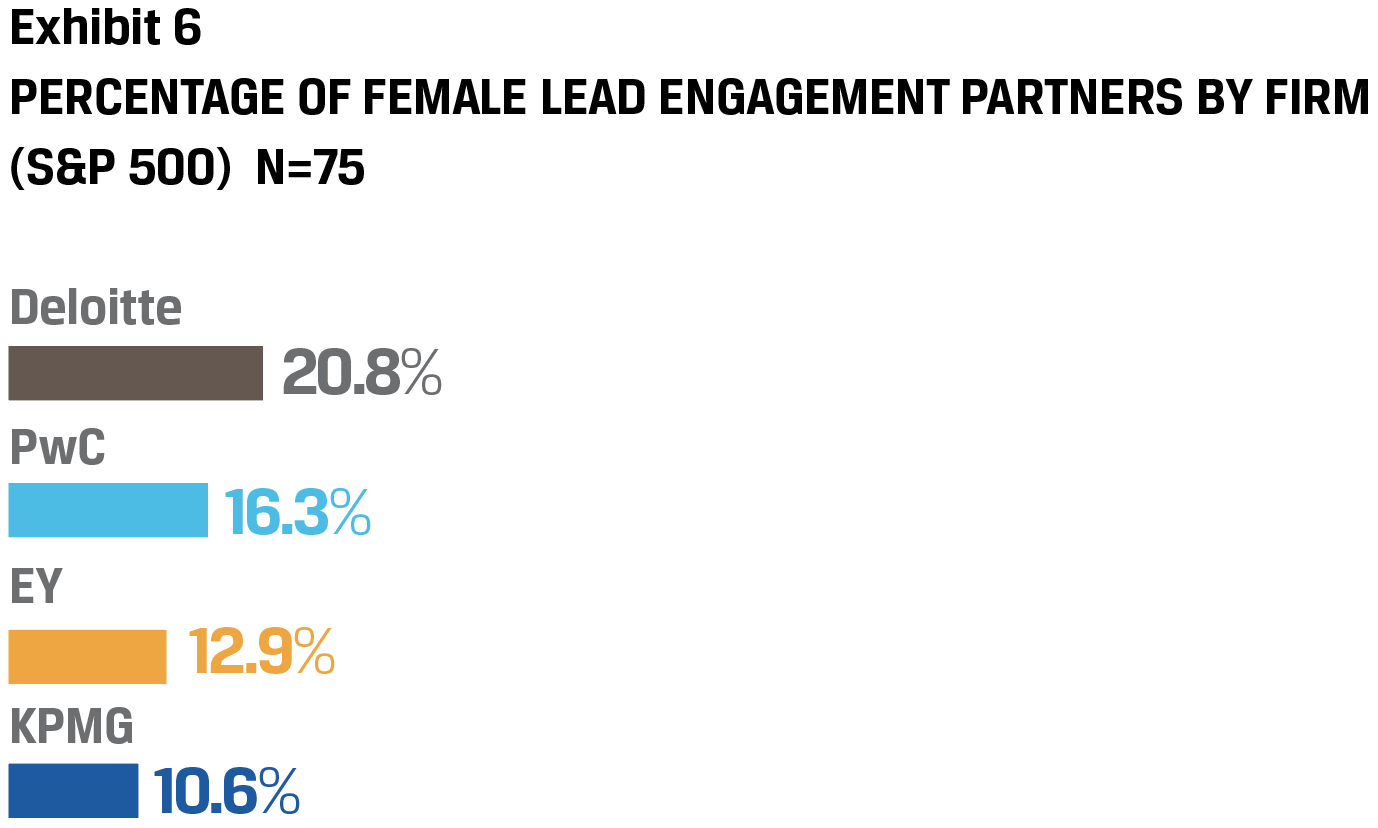

- Percentages of female lead engagement partners by S&P 500 firms were Deloitte (20.8%), PwC (16.3%), EY (12.9%), and KPMG (10.6%)

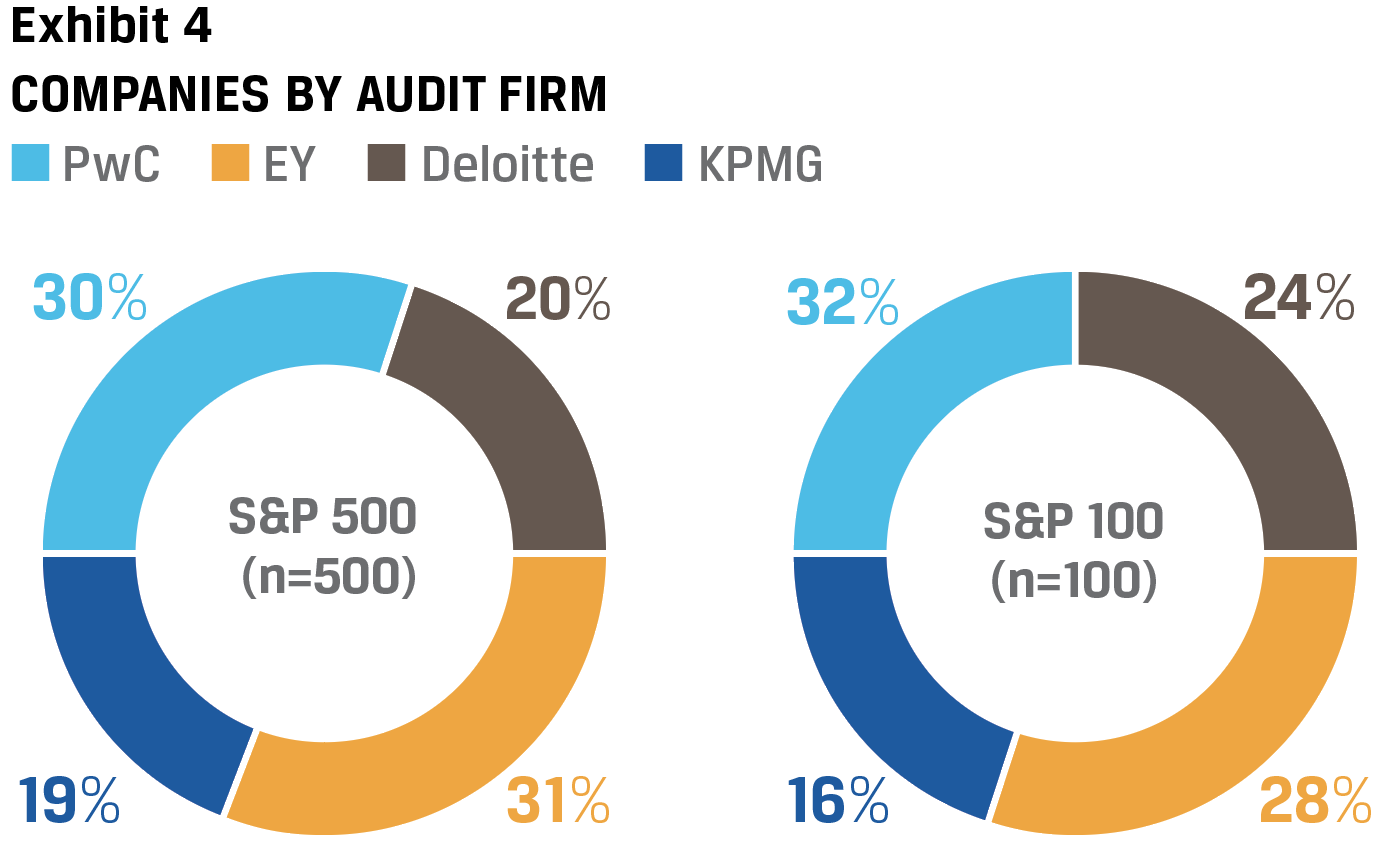

- 30% of the S&P 500 were audited by PwC, 31% by EY, 20% by Deloitte, and 19% by KPMG

- 32% of the S&P 100 were audited by PwC, 28% by EY, 24% by Deloitte, and 16% by KPMG

- Although PwC has the greatest number of S&P 500 clients, only 16.3% of them are serviced by female lead engagement partners, behind Deloitte’s 20.8%.

- EY, with nearly the same number of S&P 500 clients as PwC, is at 12.9% female lead engagement partners.

- We found no female partners among the 36 longest tenured engagements (those over 75 years) in the S&P 500

- We found only 6 female partners in the 107 companies with auditor relationships exceeding 40 years.

With this being the first year of information, our initial work is foundational. Numerous extensions will be explored in future periods.

New Standards Provide Transparency on Audits and Auditors

Over the last decade, investors told audit regulators in the United States they wanted to know more about those involved in the audit of the companies in which they invest.

They also indicated they wanted to hear directly from auditors regarding the key issues they faced in performance of the audit. To that end, the Public Company Accounting Oversight Board (PCAOB), the organization that regulates public company auditors in the United States, passed rules that strive to provide greater transparency to investors on these issues. Recently, CFA Institute published a blog post, “Audit Reports: A New Era of Enhanced Reporting”, that includes our conversation about these changes with then PCAOB Chairman James Doty. Doty indicated the changes were made to increase the credibility of auditors and the relevance of the audit report to investors. Doty highlighted that the PCAOB’s due process revealed that investors, in a post-financial crisis era, wanted more than the pass/fail model of reporting from auditors.

The first change, the Auditor Reporting of Certain Audit Participants (Audit Participants Standard), was approved for release by the SEC in 2016. The requirements commenced in early 2017, but a full complement of data was not available until the filing of 2017 annual reports in early 2018. Under this new standard, investors can now not only identify the audit firm issuing the opinion, but also the partner assigned to the engagement and to what degree other auditors were used by the primary auditor in reaching its conclusion on the financial statements. This information is now available to investors on the PCAOB’s AuditorSearch database by company name or ticker symbol.

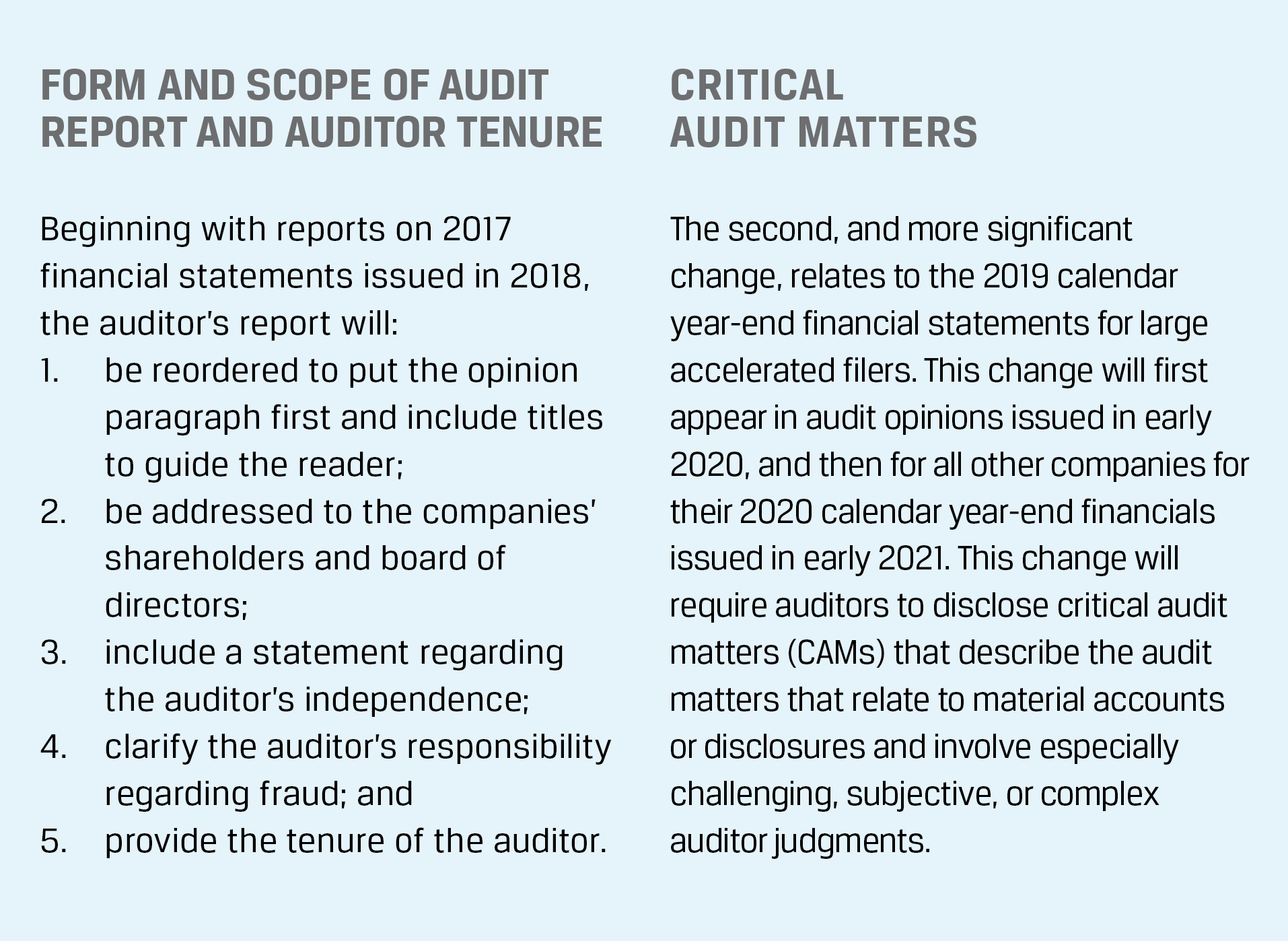

The second change, The Auditor’s Report on an Audit of Financial Statements When the Auditor Expresses an Unqualified Opinion (New Audit Reporting Standard), was approved by the SEC in October 2017 and includes changes that can be divided into two categories.

Overall, the New Audit Reporting Standard and the Audit Participants Standard seek to increase the transparency for investors as to who is involved in the execution of the audit, the duration of the auditor’s relationship with the company, and the key issues the auditor faced when executing the audit.

Exploring the Increased Transparency

Although disclosures regarding CAMs will not be available until 2020, CFA Institute reviewed several of the transparency elements currently available to determine if the data provided overall, not company specific, insights for investors. Specifically, CFA Institute reviewed lead engagement partner and auditor tenure data for insights.

Using the full complement of information from the PCAOB’s AuditorSearch database, CFA identified the names of the lead engagement partners of companies comprising the Standard & Poor’s 500 Index (S&P 500). Such information was not fully available until April 2018 due to the effective date of the Audit Participants Standard. We used CalcBench to source the audit tenure of these same S&P 500 companies. With auditor tenure now available on the face of the audit opinion, CalcBench has written a program to read auditor opinions—though they are not tagged in eXtensible Business Reporting Language (XBRL) — and pull and structure such information. We supplemented this data with manual verification. Because audit tenure was not required for all companies with a year-end prior to 15 December 2017, only 409 of the S&P 500 companies had provided such information as of the writing of this report. For 91 companies with fiscal year-ends prior to that date, the information will not be available until the end of 2018.1

Our observations from the review of the data follow.

Audit Participants

Investors told the PCAOB through its direct outreach, as noted above, and CFA Institute in our numerous surveys over the last decade, that they wanted to know more about the lead engagement partner assigned to the company in which they invest and the involvement of other auditors.

Investors have expressed their interest in the name of the lead engagement partner not only because this is something that is available on the face of the auditor’s report in other parts of the world, but because of the behavioral implications—namely accountability and increased audit quality—they perceive emanate from such identification. Investors indicate they view the naming of the audit partner as no different than the identification of the chief financial officer, the controller, or the chief executive officer for the companies in which they invest. Company management also supported the naming of the lead engagement partner. Although investors wanted the name of the lead audit partner disclosed on the face of the audit opinion, the PCAOB compromise was to include the partner’s name in the PCAOB’s AuditorSearch database.

Also included in the AuditorSearch database is the percentage of investee companies audited by participating firms. Investors told regulators that they wanted to know the percentage of companies audited by other auditors. Investors have come to recognize, through previous financial scandals, that the Big 4 firms (PricewaterhouseCoopers [PwC], Ernst & Young [EY], KPMG LLP [KPMG], and Deloitte & Touche [Deloitte]) are composed of affiliated firms, which are legally distinct entities, from across the globe. Because of this, investors want to know what percentage of the companies in which they invest are audited by such affiliated firms. The extent to which other participants are involved in the audit is a subject we will leave for another publication, but it is of equal importance to investors.

The Gender Gap: Transparency Resulting from New Audit Participants Disclosure

US Lead Engagement Partner Disclosures Highlight Gender Gap

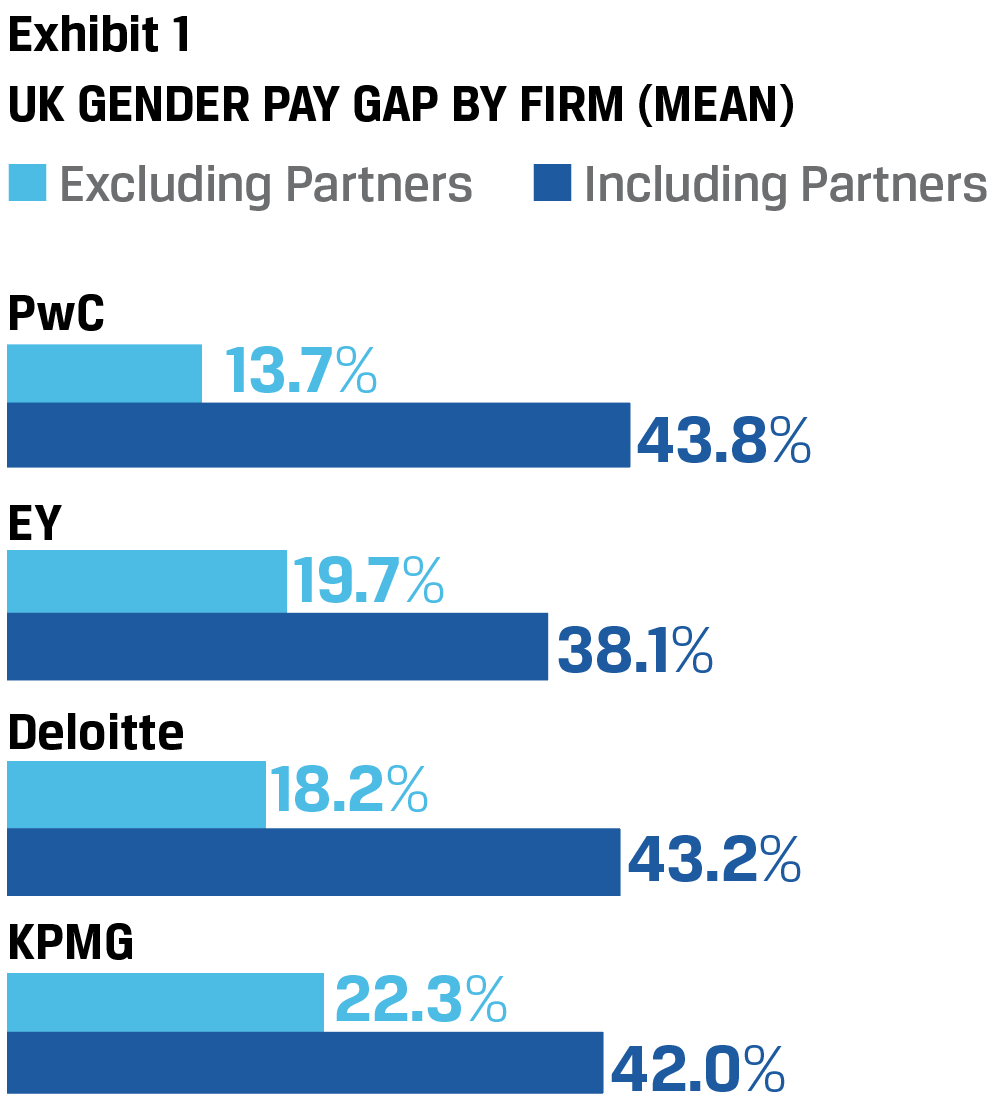

Just as the full complement of the information finally became available in the AuditorSearch database and we commenced review of the information, the UK affiliates of the Big 4 firms began to release the newly statutory required United Kingdom gender pay gap reports.

The initial pay gap reports drew a great deal of media attention because the reports from the Big 4 firms were completed, in compliance with the United Kingdom requirements, without partner statistics—because partners are owners, not employees. Laudably, the Big 4 firms voluntarily agreed to revise the reports to include partners. When including partners, the pay gaps rose substantially, as noted in Exhibit 1.

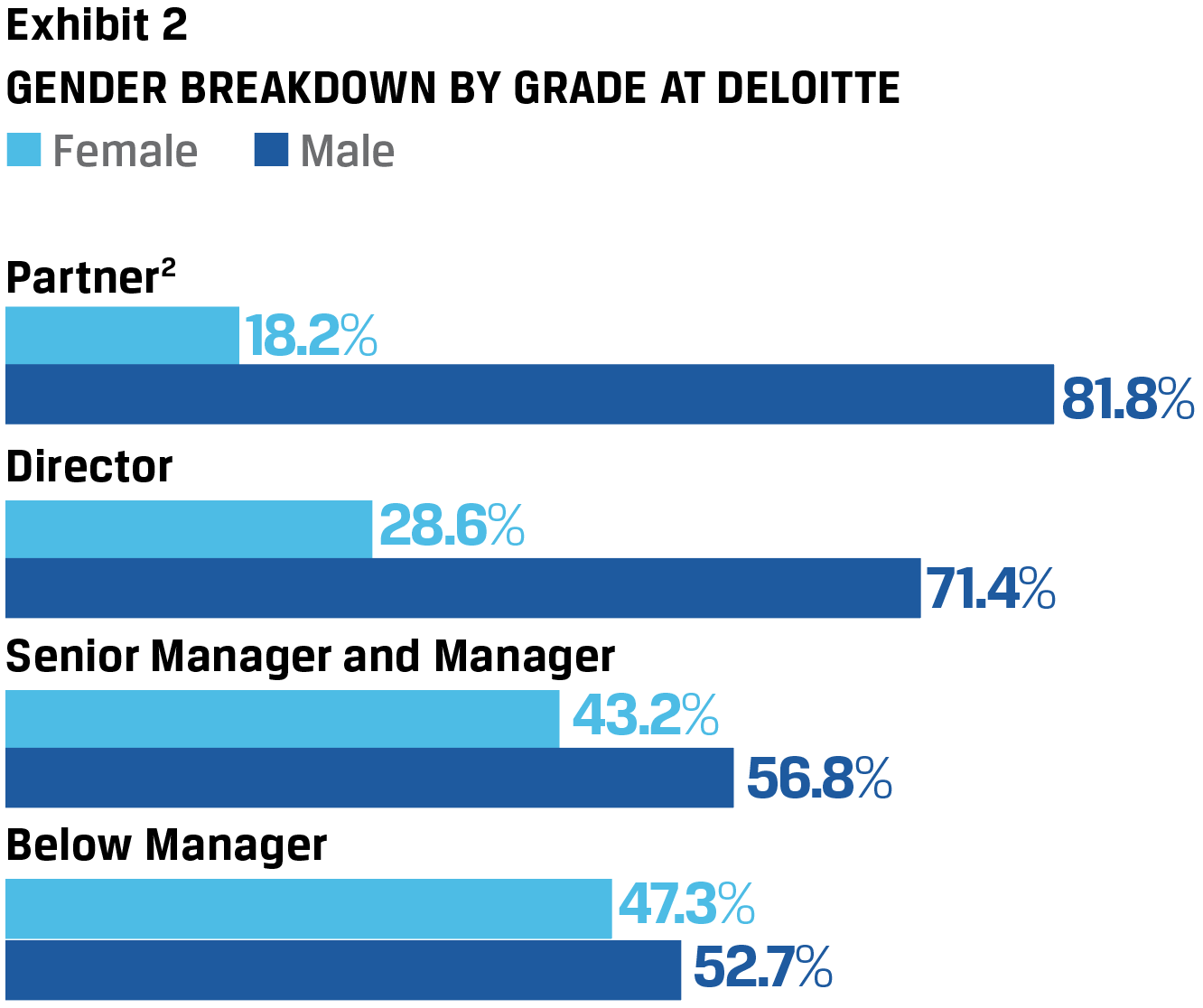

The firms attributed the even larger disparity to the much larger percentage of male versus female partners. Although the reports don’t provide specific statistics on the number of male and female partners, Deloitte’s pay gap report illustrates the attrition of women in its ranks as they rise from staff to partner. As seen in Exhibit 2, 47.3% of staff level positions are held by women, while only 18.2% of partners are women.

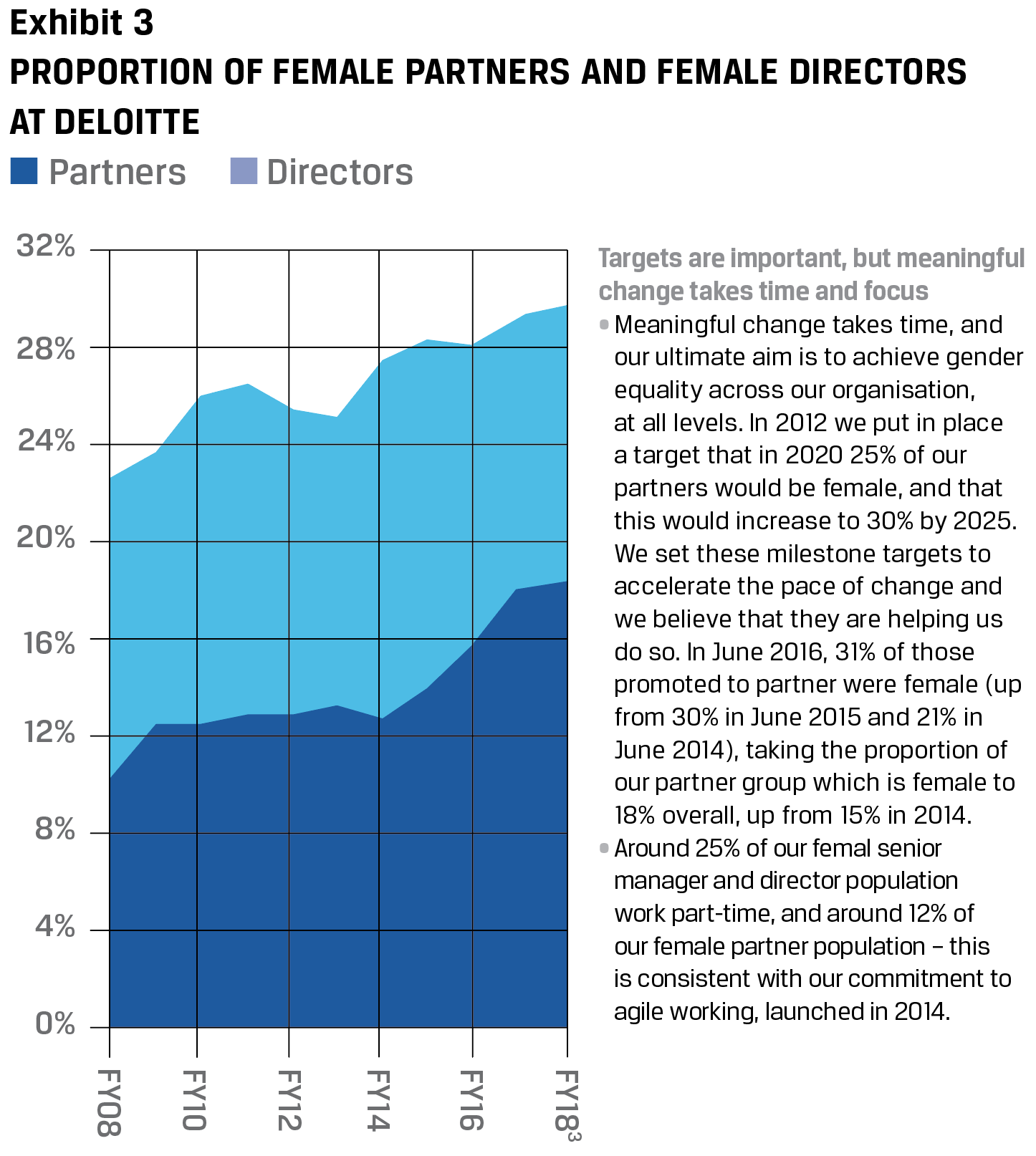

Deloitte has acknowledged the need to do better. Exhibit 3 charts its progress over the last decade and its goals going forward.

We did not note similar information in the reports from the other Big 4 firms, so it is not possible to assess the male-to-female partner ratio tilting the statistics across Big 4 firms within the United Kingdom. Although such pay gap reports are not required or available in the United States, gender diversity is something the PCAOB’s new AuditorSearch database allows investors to observe related to audits of US public companies. Having pulled the lead engagement partner names of the S&P 500 companies—audit assignments that are among the most coveted within the Big 4 firms because of the name recognition and lucrative nature of such engagements to the firms—we made the observations that follow. We also narrowed our sample to the companies in the S&P 100 to discern if there were any differences among the smaller number of even larger organizations.

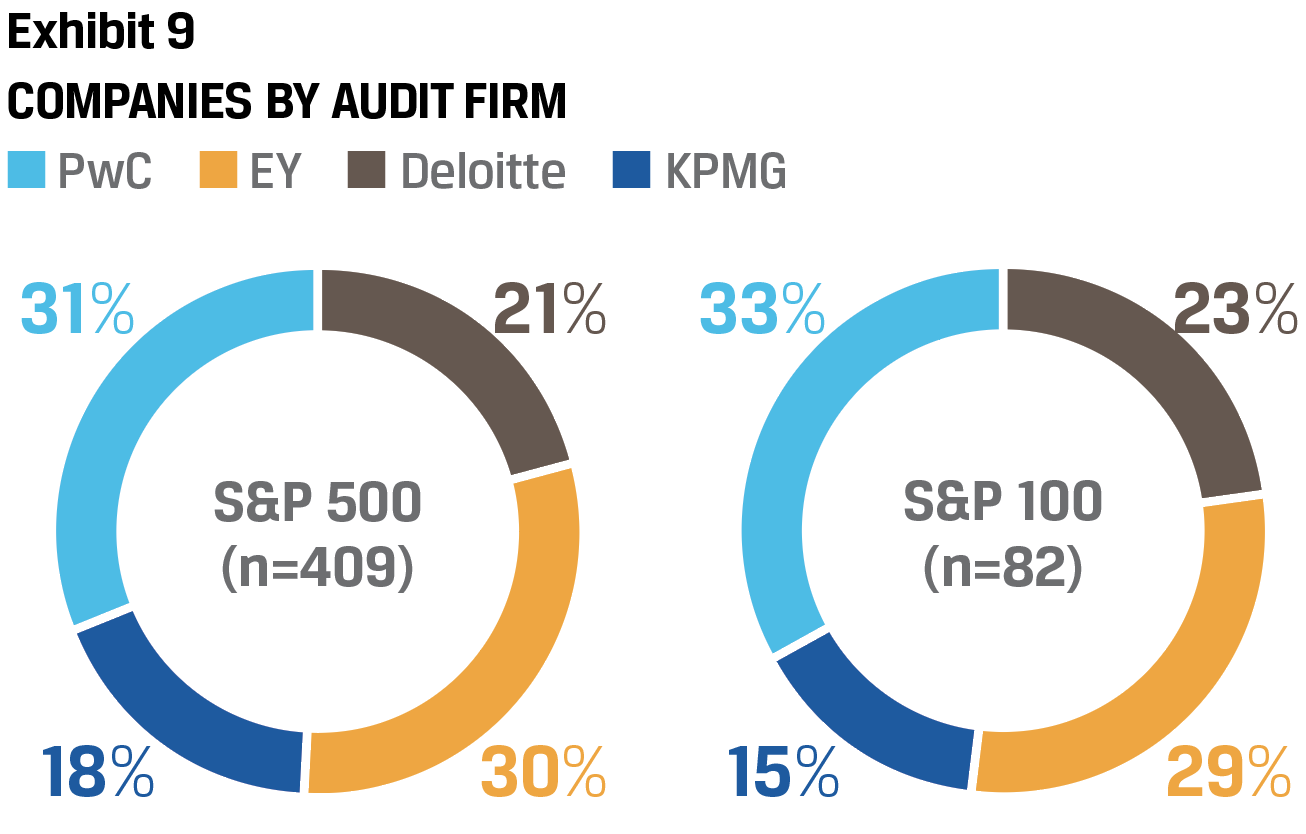

We first noted the percentage of the S&P 500 and S&P 100 companies audited by each of the Big 4 firms. The distribution of companies by Big 4 firm exists in virtually the same proportions for the S&P 500 and S&P 100. PwC (30% and 32%) and EY (31% and 28%) lead the pack, followed by Deloitte (20% and 24%) and KPMG (19% and 16%) (see Exhibit 4). Three audits of the S&P 500 companies are executed by firms other than the Big 4.

We then considered what proportion of lead engagement partners were male and female by S&P 500 and S&P 100 companies. We found that only 15% (n=75) of lead engagement partners of the S&P 500, and only 11% (n=11) of the S&P 100 were female (see Exhibit 5). This illustrates a further decrease (27%) in the representation of female lead engagement partners on the largest companies in the S&P.

There are 70 unique female lead engagement partners of the S&P 500, as five have more than one engagement (two at EY, two at PwC, one at Deloitte, and none at KPMG). No female lead engagement partner had more than one engagement in the S&P 100. We then considered the proportion of female lead engagement partners for the S&P 500 by Big 4 firm. Our results are shown in Exhibit 6.

The disparity between the firms in the percentage of female lead engagement partners in the S&P 500 by Big 4 firm was most striking. Deloitte’s percentage, 20.8 %, was nearly double that of KPMG at 10.6%. The two firms with the smallest number of S&P 500 clients have strikingly different percentages of women on their largest public company audits.

Interestingly, the US firms of Deloitte and KPMG were the first to appoint women to lead their firms in 2015. Deloitte has long been known for its conscious effort to mentor and promote women into leadership positions, as the aforementioned excerpts from their UK report illustrate. In 2018, EY will have a female CEO for the first time and Deloitte has recently announced it first female CEO will not be nominated by its board for reelection to the position in 2019.

Although PwC has the greatest number of S&P 500 clients, only 16.3% of them are serviced by female lead engagement partners, behind Deloitte’s 20.8%. EY, with nearly the same number of S&P 500 clients as PwC, is at 12.9% female lead engagement partners. These two organizations hold the greatest market share in the S&P 500. With this in mind, Deloitte stands out for the fact that even with a smaller client base, it has been relatively more successful at advancing women on to these engagements. That changes when you consider the same information for the S&P 100 (see Exhibit 7).

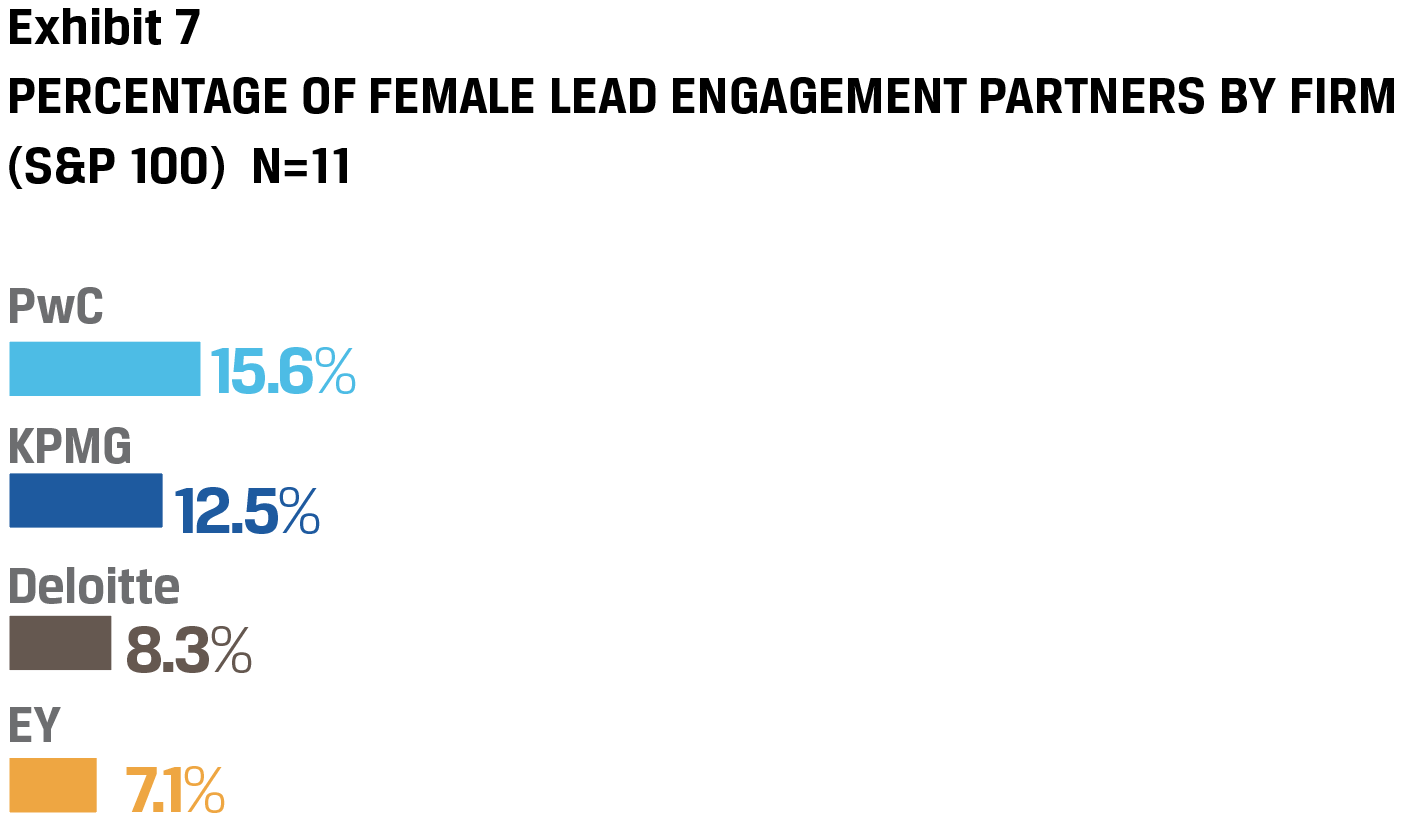

Although the firms retain relatively similar percentages of the S&P 100, substantially different results are seen not just in total percentage, 11% versus 15% from the S&P 500, but by firm. PwC’s percentage of female lead partners stays relatively consistent at 15.6% (n= 5). This puts PwC in the lead while Deloitte falls to 8.3% (n=2). Also making a precipitous drop is EY with only 7.1% (n=2) of lead engagement partners who are female. KPMG’s percentage rises to 12.8% (n=2). With only 11 female lead engagement partners in the S&P 100, a single woman can alter the statistics substantially. Overall, this confirms that women are substantially less well represented as lead engagement partners on the largest US public companies.

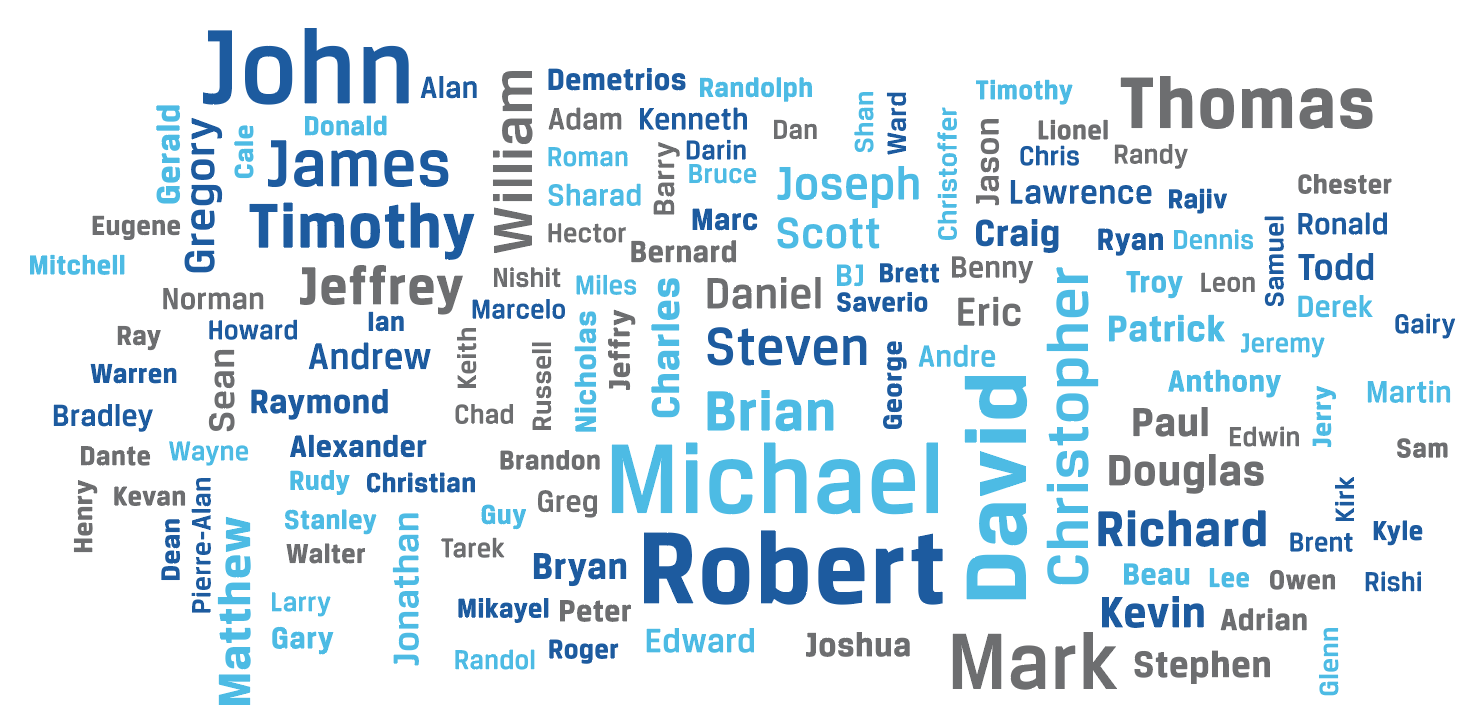

As we prepared this report, a 24 April 2018 New York Times article, “The Top Jobs Where Women Are Outnumbered by Men Named John”, intrigued us into exploring whether this might be true among lead audit partners. Men named “John,” who only represent 3.3% of the male population in the United States, are disproportionately represented among lead audit partners, accounting for 29, or 6%, of all partners and 7% of all male partners. Men named “Robert” (23) and “Michael” (22)—the next most popular US male names at 3.1% and 2.6%—are also disproportionately represented, accounting for 5% each of male partners. Collectively, the number of John, Robert, and Michael male partners (74) is nearly equal to the number of female partners (75).

Anecdotally, we observed that there may be differences by industry and geography, but we will have to extend our research further to confirm our impressions. A scan of all partner names indicates that exploration of ethnic diversity is also something to consider as a further extension of this work

Should Gender Diversity of Lead Engagement Partners Matter to Investors?

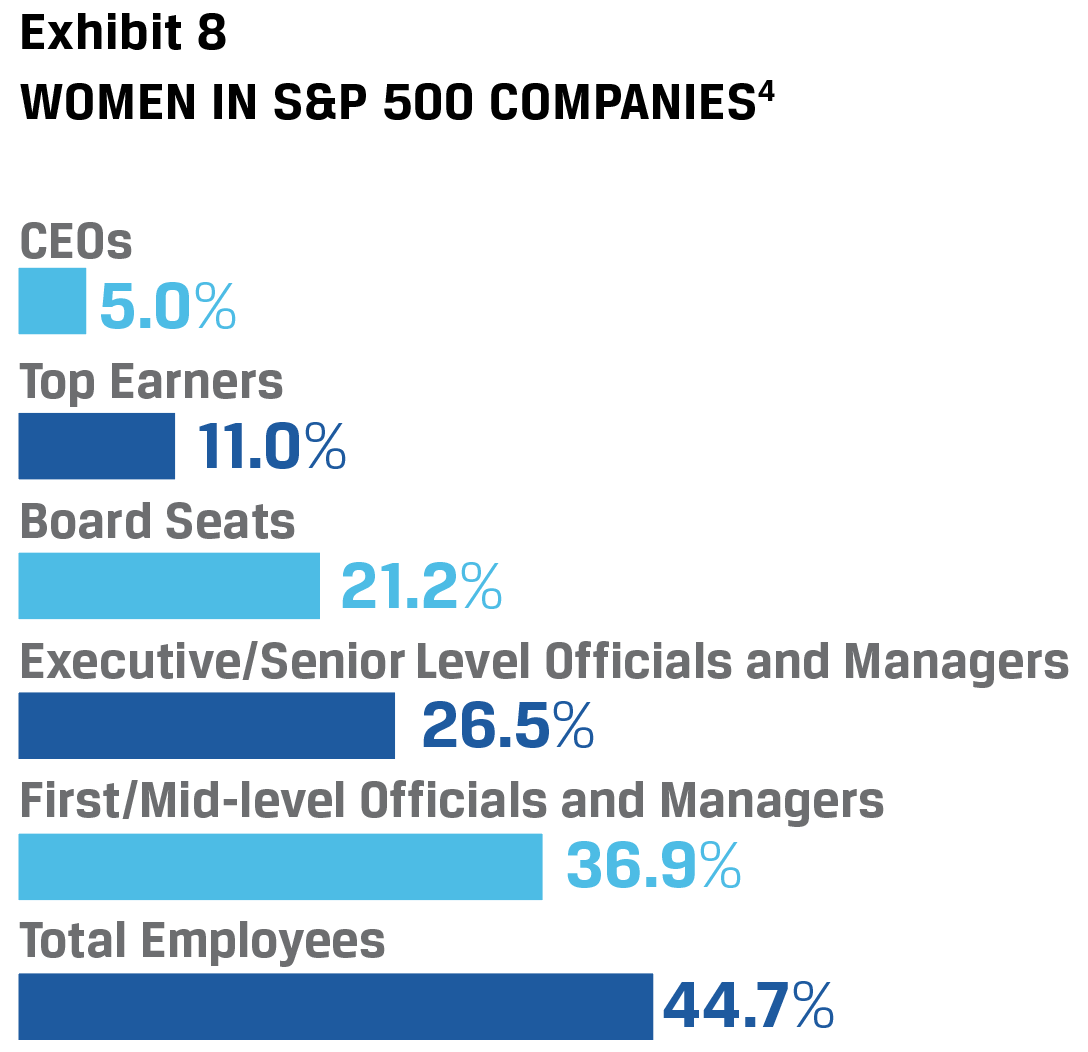

Comparing these lead engagement partner statistics to other statistics for the S&P 500 from Catalyst, we note that 5.0% of S&P 500 CEOs are women, 11% of top earners are women, and 21.2% of board seats in S&P 500 companies are held by women (see Exhibit 8). The number of female CFOs is not separately tabulated, but it would seem reasonable to assume the CFOs are in the 11% of top earners category. That said, this category also likely includes executive positions commonly populated by women, such as human resource executives.

As it relates to the Fortune 500, we note that 12.5% of the Fortune 500 CFOs in 2017 (Journey to CFO: What’s Changed for Women in 2017, Deloitte) were female and 5% of Fortune 500 CEOs (Fortune) were female as of early 2018.

With 15% of women acting as lead engagement partners for S&P 500 companies and 11% holding that role for S&P 100 companies, female representation is better than that seen for CEOs at the companies, but not as good as the percentage of women on corporate boards (21.2%)—a top priority of investors. Investors have sought greater board as well as management diversity because a broad array of research suggests a diversity of perspectives produces better outcomes for investors. Further, such diversity reflects the corporate and social responsibility objectives that many investors seek to support, particularly in light of investor desires to manage public pension funds where such corporate and social responsibility, as well as human capital management issues, are particularly important. Also important for investors and boards to consider is that not just US investors invest in US companies. Social mandates, such as those that brought about gender and ethnic pay gap regulation in the United Kingdom, are considerations for global investors. Just as the audit transparency reforms were first initiated outside the United States, these other disclosures have the potential to work their way into the US ecosystem because of global investors’ pressures to consider them.

That said, the investment management industry itself has much to do to improve diversity in its own ranks. Recent studies highlight the lack of diversity of fund managers (particularly in the United States) and the potential that women may produce slightly higher returns because of their risk-averse nature, lower trading proclivity, and longterm investment mindset5. The issue in the investment management industry as it relates to gender diversity differs from that of the accounting profession, specifically with regard to the pipeline by which women enter the profession. In the investment management industry, women aren’t entering the profession at the same rate as men, and some studies suggest women must be more credentialed to be credible. This perceived obstacle to entry is something CFA Institute is seeking to improve through its Women in Investment Management initiative.

Women enter the accounting profession at rates similar to those for men. According to a 2008 AICPA Trend Report, new graduates hired by CPA firms in 2000 were 56% female and 44% male. AICPA’s 2017 Trends Report illustrates that over the last decade, the number of female hires by US accounting firms has decreased from a slight majority of 52% to a slight minority at 48%. The Deloitte report referenced above visually illustrates that leakage of the pipeline, rather than input into the pipeline, seems to be the problem for the Big 4 firms. Within 10 to 15 years (the time it takes to be a partner), the near majority of women in accounting turns into a significant minority. The accounting profession has sought to answer this issue, but it does not seem to be substantially improving across all firms.

Although the research is inconclusive on whether women make better auditors6, the potential benefits of diversity in the boardroom, within top management of companies, and within the investment profession, would seem to apply as well for lead audit partners. Auditors are important participants in the boardroom, where investors have focused on diversity for better outcomes. Lead engagement partners participate in audit committees of the board each quarter and interact with upper management. If diversity of decision making is important to investors in the boardroom, auditors are just an extension of that interest. Further, research suggests that diverse audit committees make better auditor selection decisions. To arrive at a diverse audit committee, women must have the financial expertise to qualify to participate. Big 4 firms are a training ground for the development of the necessary skills for many such individuals, as well as a pipeline for controllers and CFOs of these large public companies. To that end, audit committees have a role to play to benefit diversity in the financial management of the organizations they oversee.

There are no definitive answers whether auditor gender matters. The PCAOB data on lead engagement partners presents an opportunity for discussion and further research on the importance of diversity on these key engagements. This first full year of data is but one data point for investors. In advocating for greater transparency, investors wanted to track changes in lead engagement partners over time. The mandatory rotation of public company lead engagement partners every five years presents an opportunity to observe, monitor and effectuate change in the number of female lead engagement partners. Unlike boards and management, lead engagement partners must change every five years, which presents an opportunity to build expertise and diversity of lead engagement partners.

Auditor Tenure

Over the last decade, investors have expressed concerns regarding lengthy audit tenures because they believe long relationships may reduce auditor objectivity. Even though engagement partners rotate, investors believe there is “stickiness” to previous judgement calls and that a fresh look by a new auditor may be necessary on an intermittent basis. Similarly, investors have also questioned the long tenure of board members at times because of the need for fresh perspectives and new skills.

Newly enacted EU laws mandate rotation of auditors every 20 years and mandatory tendering of audit engagements each decade. There was significant pushback to the initiative by companies and auditors in the United States, who predicted that costs would increase and audit quality would decrease. Investors understand those trade-offs, recognizing that ultimately they, as the owners of the companies, bear the increased cost and the risk of reduced quality. In the years to come, researchers will be able to study the effects of such transitions within the EU and validate or disprove these narratives. Ultimately, the PCAOB decided that in the United States, disclosure of the tenure of the auditor’s relationship with the company would be made in public company auditor’s opinions.

Although some organizations have previously provided auditor tenure in other disclosures, the PCAOB disclosures this year are the first provided with the audit opinion under this official guidance. As we noted above, as of the date of our research only 409 of the S&P 500 had reported tenures under the new rules because of fiscal versus calendar year-end reporting differences. Only 82 of the S&P 100 had reported for the same reason. By the end of 2018, a full complement of data should be available.

The relative proportionality of the Big 4 firms serving as auditors of the S&P 500 and S&P 100 was not altered significantly because of the difference in the number of firms reporting (Exhibit 9).

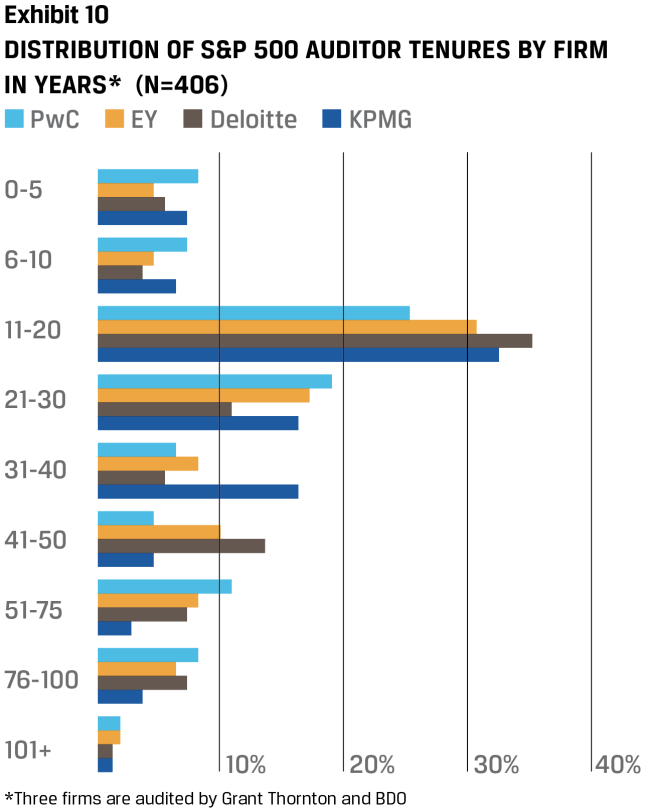

Tenures of the 409 S&P 500 companies who have reported,broken down by accounting firm, are shown in Exhibit 10.

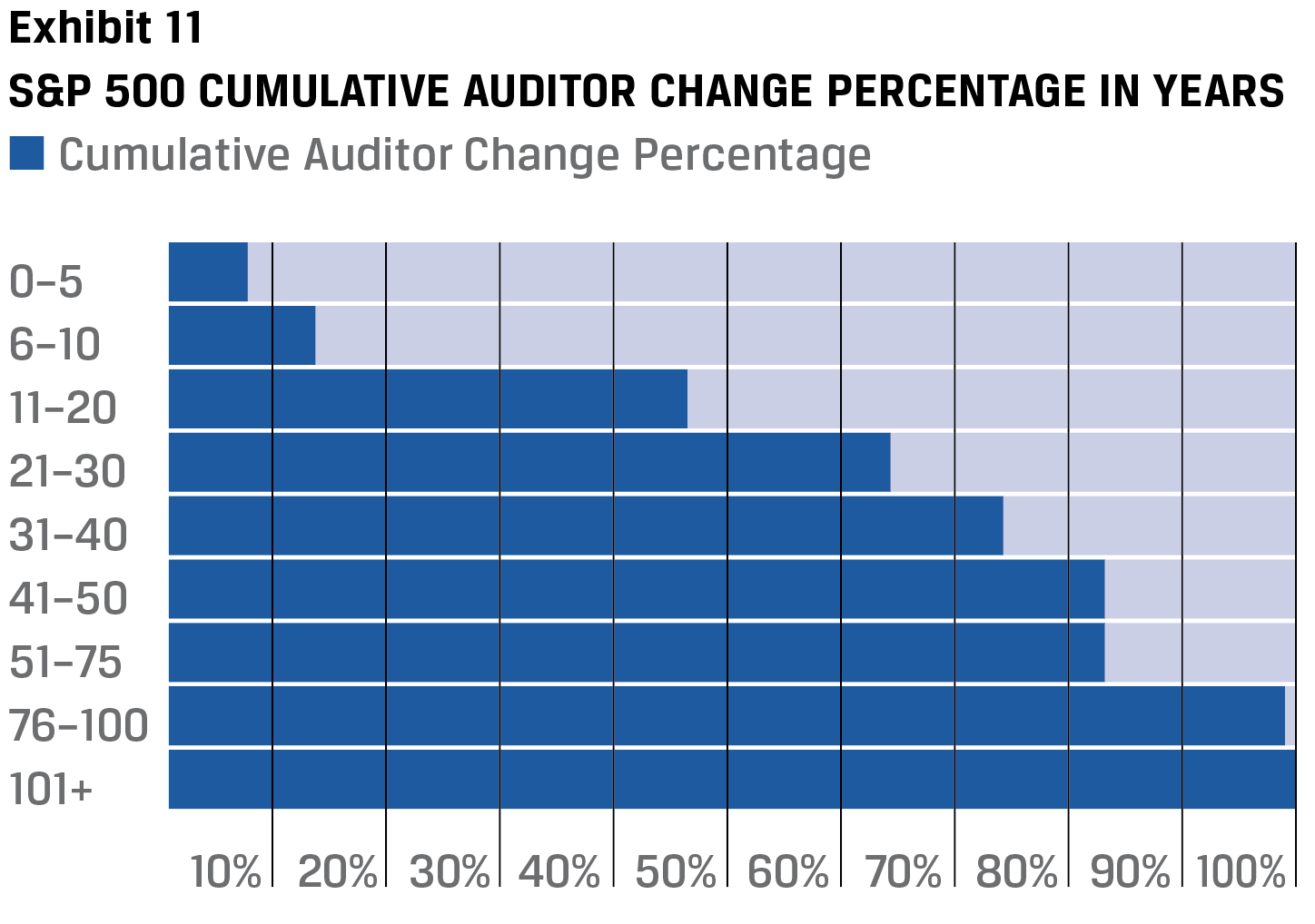

Approximately 13% of the companies (52 of 409) have changed auditors in the last 10 years, with only approximately 6–7% changing in each of the most recent five-year periods. The demise of Arthur Andersen in 2002 can be seen to be the major contributor to the significant number of tenures in the 11–20 year category, with nearly 34% of the relationships changing in that timeframe (Exhibit 10). Approximately 54% of the companies have a relationship more than 20 years in duration and nearly 18% have relationships of more than 50 years. Generally, less than 10% of companies change auditors every decade. Exhibit 11 shows the cumulative percentage change in auditors over time.

The companies and auditors with relationships of more than 100 years include those shown in Exhibit 12.

In doing our research we found only a handful of companies that had changed auditors in the last three years (the period covered by the opinions in the Form 10-K).

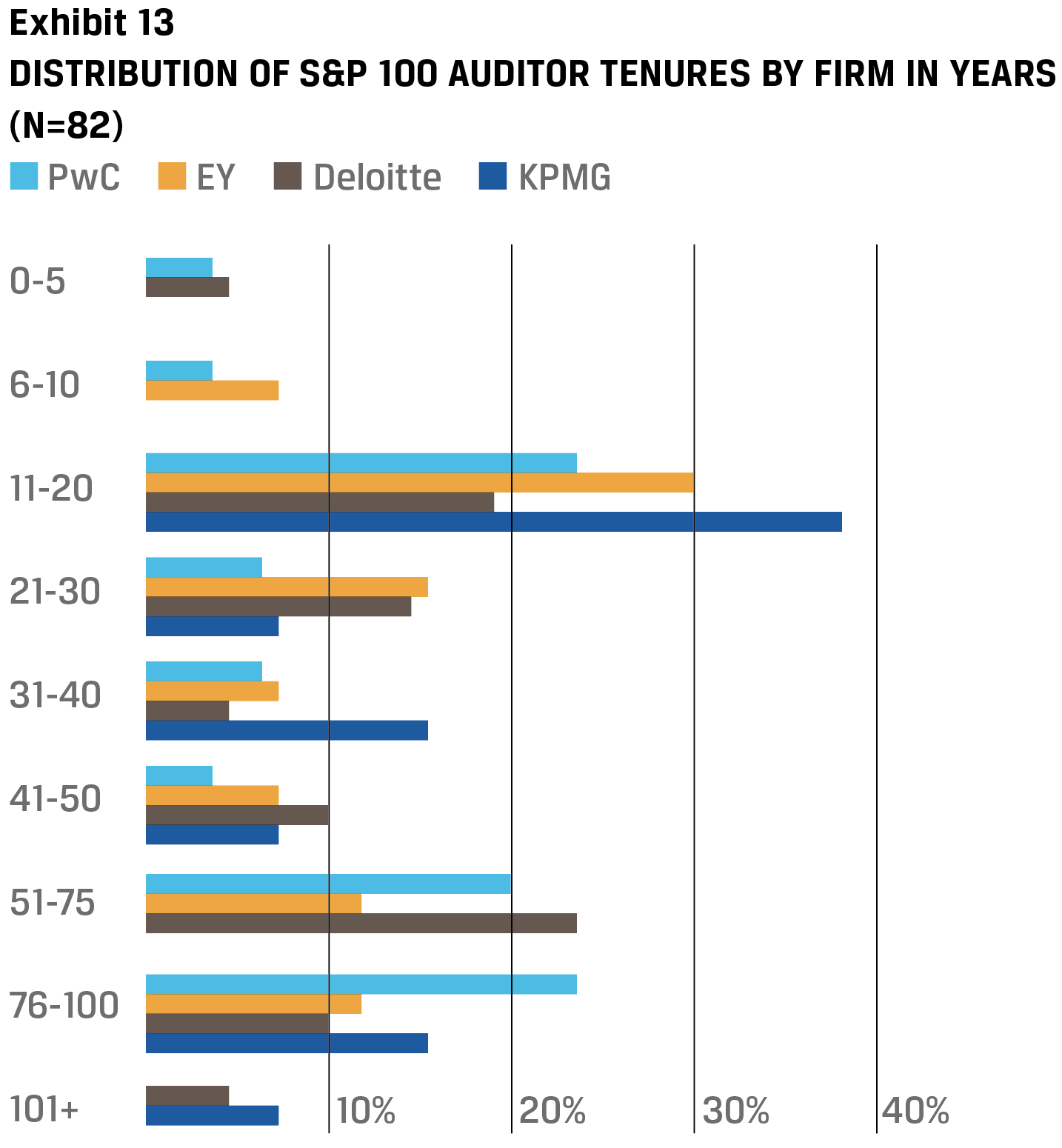

Applying this same analysis to the S&P 100, we find an even lower turnover of auditors (Exhibit 13).

Only 5 of the 82 companies, or approximately 6%, have changed auditors in the last 10 years, with only approximately 2-4% changing in each of the most recent five-year periods. As it was for the S&P

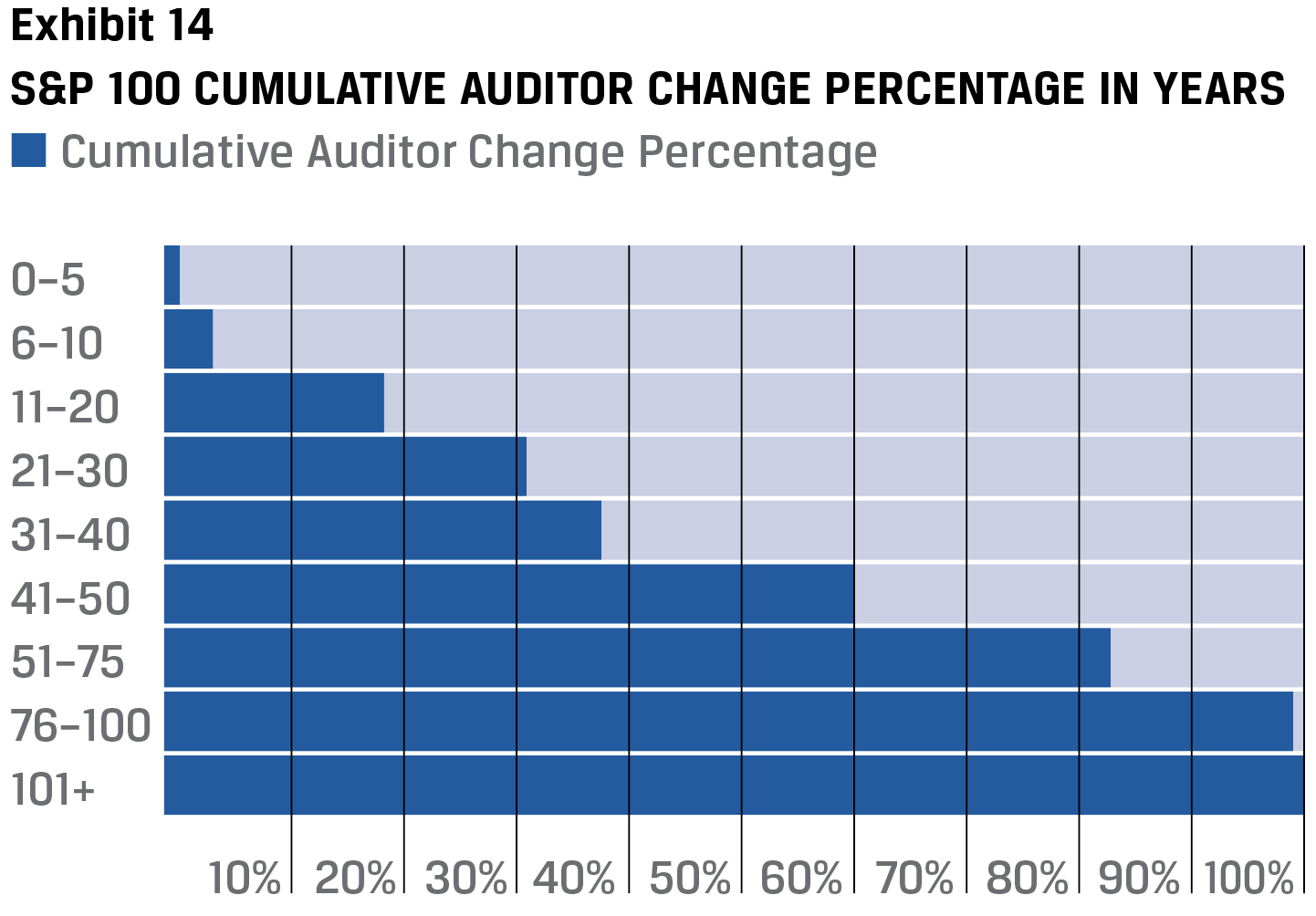

500, the demise of Arthur Andersen in 2002 can be seen to be the major contributor to the significant number of tenures in the 11–20 year category, with nearly 30% of the relationships changing in that time period (Exhibit 13). Approximately 65% of the S&P 100 (up from 54% of the S&P 500) companies have a relationship more than 20 years and nearly 37% (up from 18% of the S&P 500) have relationships of more than 50 years. Overall, less than 6–12% of companies change auditors every decade. Exhibit 14 shows the cumulative percentage change in auditors over time.

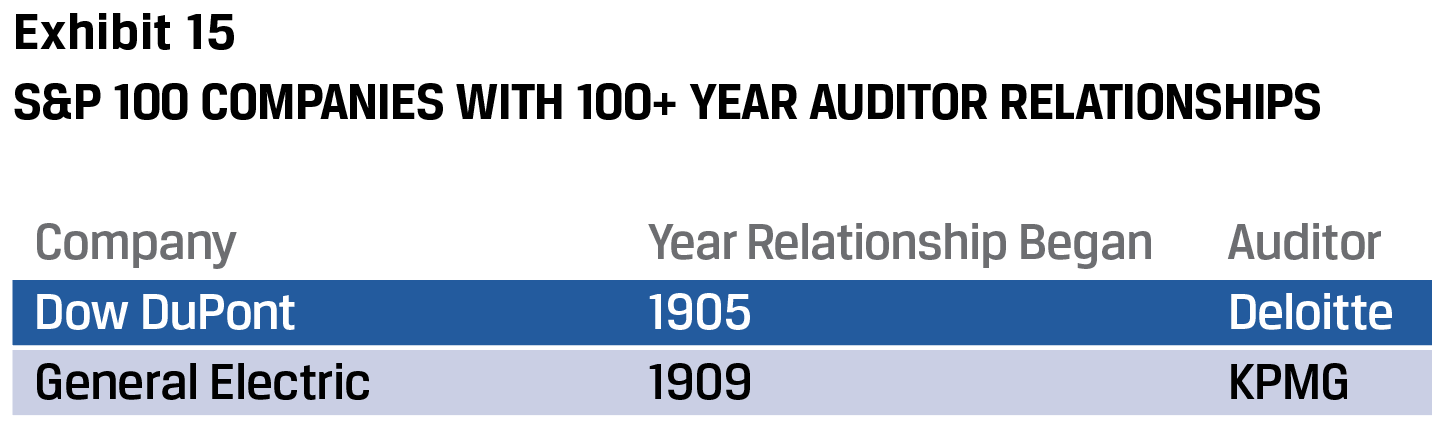

Deloitte and KPMG have both had relationships with an S&P 100 company for more than 100 years (Exhibit 15).

We then considered the Big 4 tenures as a percentage of their total number of clients to common size for the difference in numbers of clients in the S&P 500. We found generally similar tenures in percentages terms with a few anomalies by firm, indicating tenure is not a by-firm phenomena in the S&P 500. We then considered the same for the S&P 100. Interestingly, we found that PwC’s S&P 100 companies represent a significant percentage of their most tenured clients with 48% (13 of their 27 companies) of such clients being with PwC for more than 50 years. Deloitte’s S&P 100 companies with over 50 years tenure amounts to 42% (8 of their 19 companies). KPMG and EY’s most tenured clients in the S&P 100 only represented 25-26% of their S&P 100 relationships. With higher percentages in the 11-20 year categories, the data may suggest they benefited most from the movement of S&P 100 companies from Arthur Andersen.

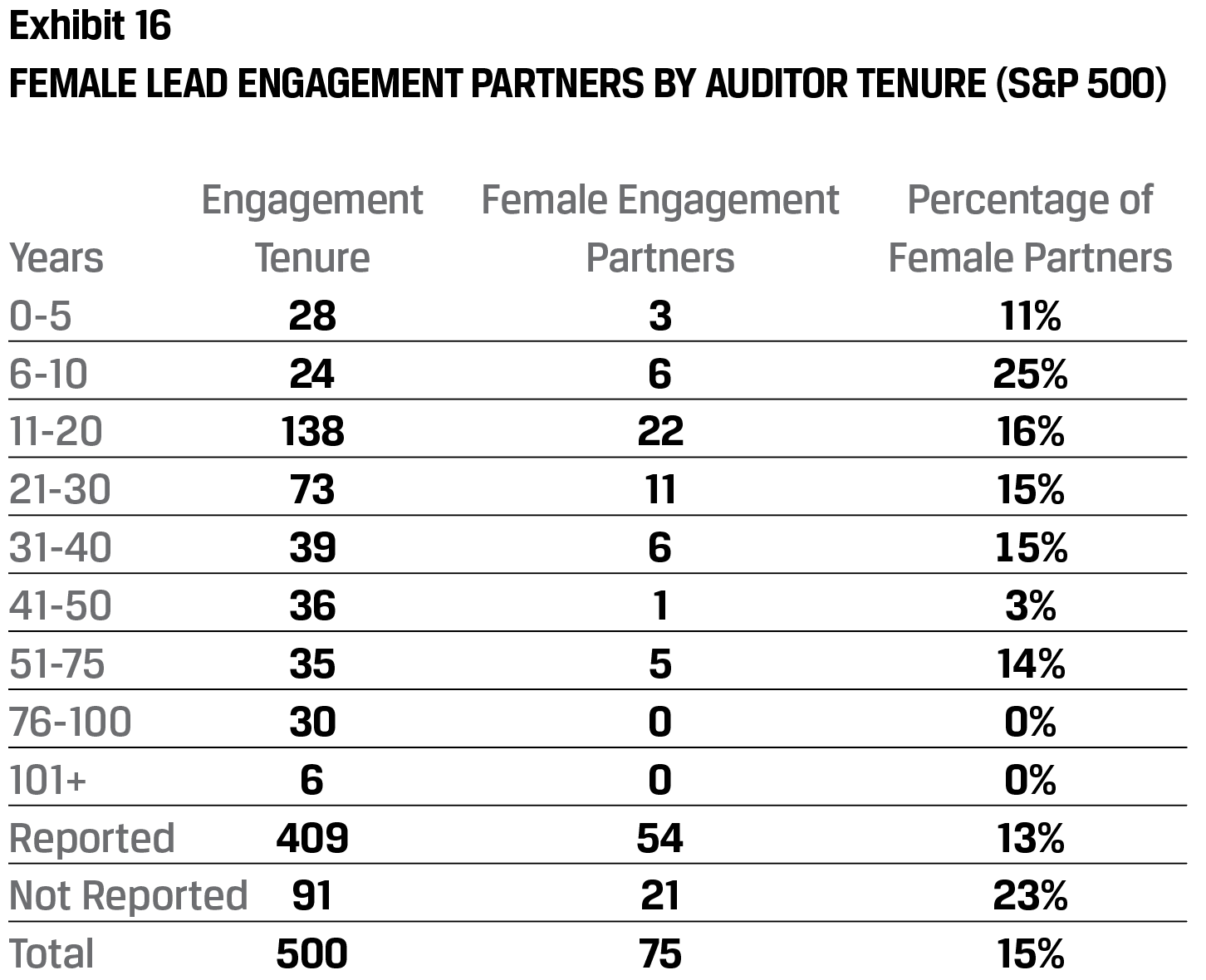

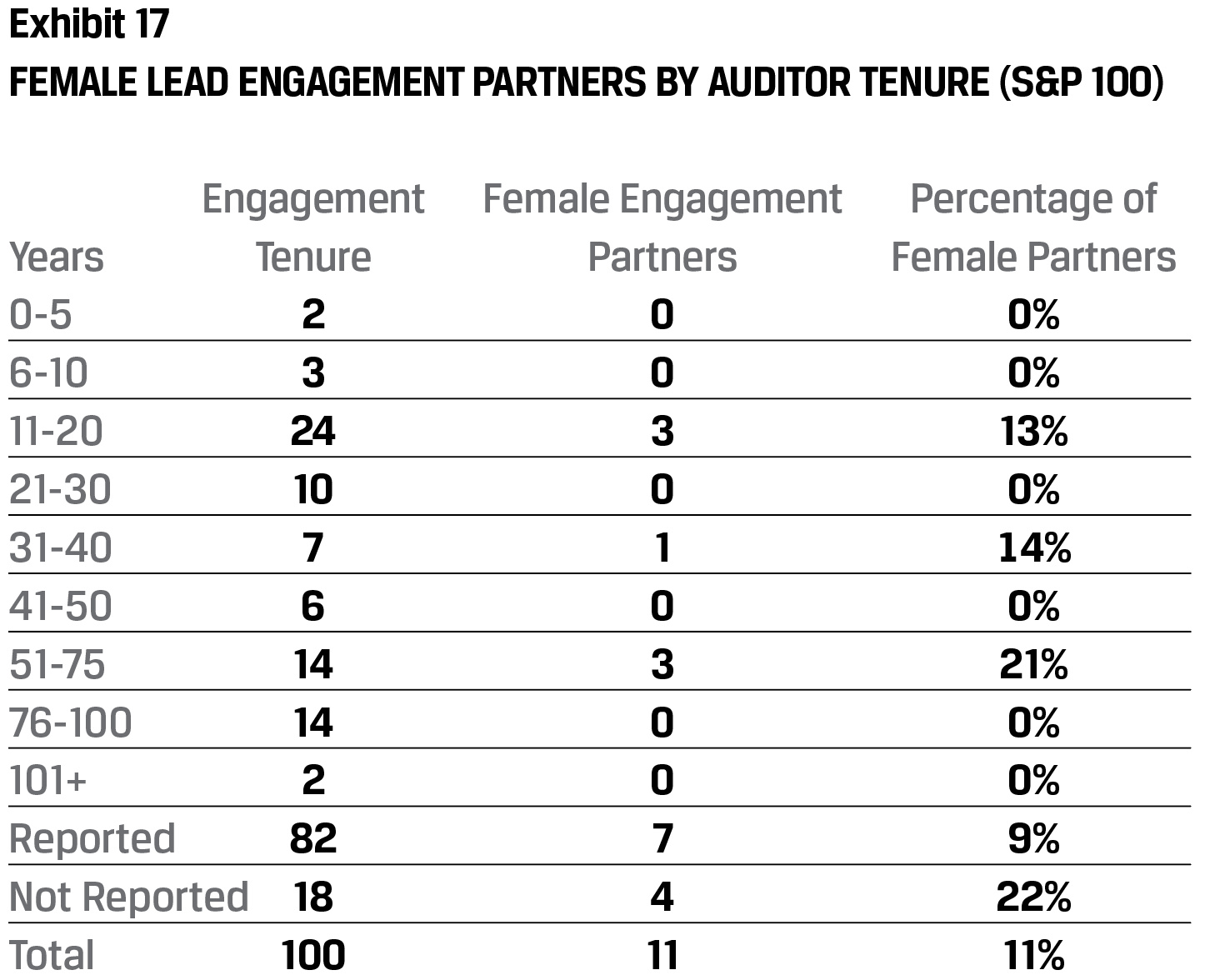

Out of interest, we also considered whether any relationship existed between auditor tenure and number of female lead engagement partners in the S&P 500. We found no female partners among the 36 longest tenured engagements (those over 75 years) in the S&P 500 and only six female partners (5.6%) in the 107 companies (26% of total companies) with auditor relationships exceeding 40 years. We performed the same analysis of the S&P 100. In terms of percentages we found a similar trend, with no female partners as lead engagement partners on engagements with relationships over 75 years and only three female partners (8.3%) as lead engagement partners on 36 companies (44% of the total companies) with tenures over 40 years. Overall, the most tenured clients are less likely than average to be staffed with a female lead engagement partner (Exhibits 16 and 17).

Interestingly, there are 21 female partners (23%) on the 91 S&P 500 firms to yet report their tenures because they have a fiscal rather than calendar year end. The same relationship exists for the S&P 100 firms. As we don’t know the tenure of those relationships, we will have to extend our research when a full complement of tenure statistics becomes available. A look at the underlying data suggests a correlation may exist between industry and female partners, but this is an extension of the research we did not fully validate through review of industry codes.

Future Extensions of This Work

With this being the first year of information, our initial work is foundational. Numerous extensions that investors will likely explore in future periods include the following:

- increased insight into diversity statistics (e.g., ethnic diversity) (based upon our preliminary analysis, there is work to be done in this area);

- consideration of differences in tenure and lead engagement partner gender by industry;

- whether corporate boards, or corporate management (e.g., CFOs) with greater diversity correlate to higher auditor diversity;

- whether various industries have significantly different tenures or percentages of women auditors; and

- analysis of the percentage of the S&P 500 audited by affiliated firms both at a point-in-time and over time.

Over time, there will be the ability to time series the information, showing

- the rotation of individual partners between engagements and firms;

- the percentage of companies who change auditors over time; and

- whether women make progress in advancing to these high-profile audit engagements.

The information provided by the transparency project disclosures will provide insight to investors on the individual elements of disclosure on the companies in which they invest and will—as illustrated with lead engagement partners disclosures—provide data for analysis and insight at an aggregate level that was not originally anticipated. Such data and analysis will also be useful to the corporate boards who serve to protect investor interests. Those boards will be able to observe the rotation of lead engagement partners and the tenure of their company’s auditor relationships relative to their peers in their industry.

We expect that data providers will build capabilities to more readily extract such information and time-series it in upcoming years extending this research as we note above. We also expect that new machine-readable programs will be developed that will assist investors with a ready comparison, between companies and years, of the yet-to-be-implemented critical audit matters disclosures.