This In Practice piece gives a practitioner’s perspective on the article “Buffett’s Alpha,” by Andrea Frazzini, David Kabiller, and Lasse Heje Pedersen, published in the Fourth Quarter 2018 issue of the Financial Analysts Journal.

What’s the Investment Issue?

The reasons for Warren Buffett’s exceptional investment success are widely debated. Advocates of the efficient market hypothesis argue that it could be the result of luck. The counterargument is that it is no coincidence that he and many other successful stock market investors have adhered to the same intellectual school of investing, the Graham and Dodd principles, which prioritise value and quality when picking stocks.

The authors set out to explain why Buffett’s investment firm, Berkshire Hathaway, has significantly outperformed the wider US stock market over the past four decades. They also consider whether Buffett’s success is primarily because of his ability to pick stocks or his skill as a CEO.

How Do the Authors Tackle the Issue?

The authors start by calculating Berkshire’s performance from 1976 to 2017: its average annual return and volatility, its Sharpe ratio (the excess return achieved per unit of risk), and its information ratio (a measure of relative risk-adjusted returns). They compare these with the Sharpe and information ratios of all other US common stocks over different periods of time, using stock return and mutual fund data from the CRSP database.

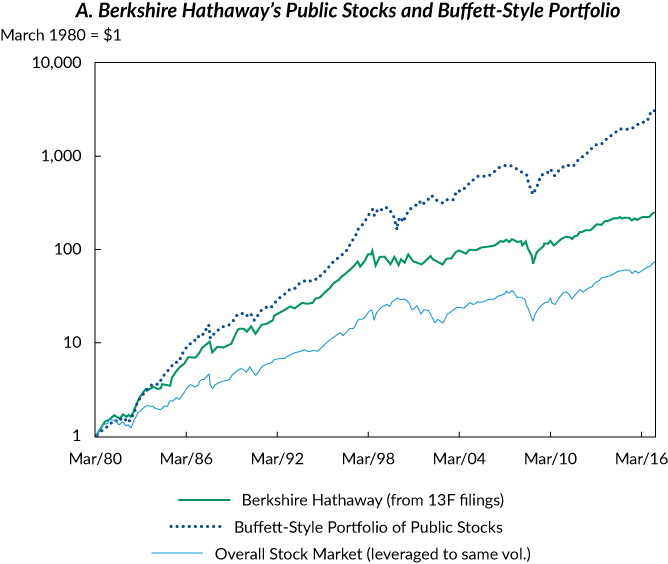

The authors then decompose Buffett’s overall returns. Using Berkshire’s 13F filings, they calculate the performance of the publicly traded companies the company has owned. They compare this performance with estimates of the performance of Berkshire’s private companies—performance that may reflect Buffett’s success as a CEO rather than just his stock-picking ability.

They study Berkshire’s balance sheets and stock price over time to determine how much leverage Buffett uses. They examine the types of leverage used: the sources, terms, and costs. They also look at the extent to which the company has benefited from favourable tax structures.

Next, the authors look at how Buffett selects companies by examining his factor exposures. They run regressions on Berkshire’s excess market return, controlling for the standard factors that capture the effects of size, value, and momentum. An innovation in this study is that the authors also control for two other factors: betting against beta (BAB), which measures the volatility of underlying stocks, and a quality factor (quality minus junk, or QMJ).

Finally, they create Buffett-style investment portfolios that attempt to replicate Berkshire’s market exposure and active stock-selection themes and are leveraged to the same active risk to see if the performance is replicable.

What Are the Findings?

Berkshire’s average annual return of 18.6% above the US T-bill rate—and far in excess of the 7.5% excess return of the market—comes with higher risk. Berkshire’s volatility of 23.5% is higher than the market volatility of 15.3%. The authors calculate a Sharpe ratio of 0.79 for Berkshire—1.6 times higher than the market’s Sharpe ratio. This, they note, is the highest of any US stock or mutual fund with a 40-year history from 1926 to 2017.

Decomposing these returns, the authors find that Berkshire’s holdings between 1980 and 2017 are, on average, 65% in private companies and 35% in public stocks. Both portfolios exceed the overall stock market in terms of average excess return and risk, but the public stocks have a higher Sharpe ratio. This result suggests that whatever value Buffett might add as a CEO, his stock-picking ability has been central to his success. The authors point out that this performance is all the more impressive given the transaction costs and possible additional taxes that Berkshire would have incurred.

By studying Berkshire’s balance sheets, the authors determine that its average leverage is about 1.7 to 1, which helps explain why Berkshire is more volatile than the wider market. They show that Buffett has developed a unique access to anomalously low-cost leverage—partly because Berkshire enjoyed easier and cheaper access to debt than its competitors, thanks to a 20-year-long AAA rating from 1989 to 2008. Another reason is that Berkshire’s insurance float (which involves collecting insurance premiums ahead of paying out claims) has a very low average cost—about 3 percentage points below the average T-bill rate. They estimate that, on average, about 35% of Berkshire’s liabilities have consisted of this low-cost insurance float.

Though the use of leverage has helped magnify Buffett’s returns, it falls far short of explaining Berkshire’s 18.6% average returns. By examining factor exposures, the authors find that Berkshire has loaded significantly on the beta and quality factors. In other words, Buffett picks stocks that are safe, cheap, and high quality. These factors almost completely explain the performance of Buffett’s public portfolio, as well as a large part of Berkshire’s overall stock return and the performance of its private portfolio. The authors note that Buffett has timed entry and exit exposure to the various positive factors and leverage over the past 40 years. The role of the private holdings is largely to provide tax benefits and cheaper access to leverage.

What Are the Implications for Investors and Investment Professionals?

This study suggests that Buffett’s exceptional performance is the result not of luck but rather of the consistent adherence to Graham and Dodd investing principles, an emphasis on value and quality exposures. Consequently, the authors provide an argument against the efficient market hypothesis.

By creating their own investment portfolios that track Berkshire’s market exposure and active stock-selection themes, the authors find they are able to achieve returns comparable to Buffett’s after transaction costs are considered. This result shows that Buffett’s extraordinary returns are not inexplicable. They require foresight and consistency that would be very difficult for another fund manager to replicate. Buffett has been able to maintain his strategy during several down years and drawdown periods without having to resort to fire sales.