Green bonds can help achieve the goal of a low-carbon world, and cumulative issuances have already reached USD1 trillion. As the market for green bonds continues to grow, investors need to understand how these instruments differ from normal bonds.

Introduction

With more than USD1 trillion of cumulative issuances, green bonds have come a long way since they originally started in 2007, because of issuances by the European Bank for Reconstruction and Development (EBRD) and the World Bank. Although the term “green bond” has no official definition, what matters when considering whether a bond is green is not the issuer but rather what the bond’s proceeds will be used for. Because of this, green bonds are generally associated with both

- the kinds of projects they are used to finance or refinance, such as projects that help in decarbonisation or in adaptation and resilience to climate change—these projects include renewable energy, mass transportation, sustainable water, waste management—and

- a specific process the bonds need to go through (a fixed-income debt instrument that needs to go through a certain governance mechanism) in order to qualify for a green label, which in some cases is verified by an external agency.

Difference between Normal and Green Bonds

The issuance of a green bond is designed to be a simple add-on to the normal bond issuance process. Table 1 shows two columns: Column A describes the regular bond issuance process that generally is initiated when the issuer decides to get rated and ends with the monitoring of the bond’s performance in the secondary market; Column B shows the simple supplementary steps that the issuer should take in order to add the green layer to the bond.

Table 1. Steps Involved in Issuing Green Bonds

|

Issuing a Regular Bond (A) |

Issuing a Green Bond—Additional Steps (B) |

|

Pre-issuance Get rated Get market intelligence on currency, tenor, size Decide on underwriters Register with local regulator Issue prospectus Comfort letter/due diligence Outreach through road shows and sales |

Pre-issuance Define a green bond framework Define how project meets green bond eligibility criteria (use of proceeds) Put in place project selection process and select eligible projects (selection of projects and assets) Set up accounts and process to earmark and allocate proceeds—“ring fence” the proceeds (management of proceeds) Establish reporting processes Get pre-issuance external review (external review) |

|

Launch the bond into the market |

|

|

Post-issuance Price and allocate bond to support secondary market performance Communication to the capital market Monitor secondary market |

Post-issuance Allocate proceeds to the projects Monitor the projects Publish impact report Post-issuance audit if necessary |

As Table 1 shows, the regular bond issuance process (A) and the green bond issuance process (B) can take place concurrently. Before and after the launch of the bond in the market, the issuer should set up certain internal procedures that correspond to the pre-issuance and to the post-issuance phases, respectively.

The processes of a green bond issuance do not significantly vary with either the nature of the issuer (for instance, corporate, sovereign, or semi-sovereign) or the bond type (such as a use-of-proceeds bond, project bond, or sovereign bond). These processes are now widely understood by investors and the market. The additional steps are explained in the following subsections.

Step 1. Preparation of a Green Bond Framework

A green bond framework is a document that discusses how the issuer’s processes meet commonly accepted green bond eligibility criteria. These processes include those implemented during pre-issuance (use of proceeds, selection of projects and assets, management of proceeds, external review) and those implemented in the post-issuance stage (post-issuance audit and reporting). An issuer’s green bond framework is a public document and is considered the centrepiece of the issuance process. Although there is no uniform prescribed way to write the framework, it reflects the four pillars of the green bond principles, which are also fully integrated in the Climate Bonds Standard. Thus, a green bond framework typically has four sections: preparation, use of proceeds, selection of projects, and selection of assets.

Preparation

The issuer of a green bond should establish, document, and maintain an internal decision-making process that it will use to determine the eligibility of the underlying projects and assets (use of proceeds, selection of projects and assets, management of proceeds, reporting). This process begins with a statement regarding the green bond’s environmental objectives, reflected in the “Introduction” or “Overview” section of the framework document.

This aspect of the issuance process is very important because it provides issuers the opportunity to directly explain to investors why and how green bonds fit within their long-term vision or corporate strategy. For instance, the government of Nigeria issued a green bond in December 2017 that was ultimately certified under the Climate Bonds Standard. The government used the bond issuance to signal to the market its use of green bonds as a tool to fund its emissions reductions targets under the Paris Agreement.

Use of proceeds

The main additional requirement for a green bond compared with a vanilla bond is that the proceeds are allocated to “green” projects and assets. It is therefore crucial that the issuer clearly identify the categories of “green” that are considered eligible for inclusion in the bond.

These categories are linked to the nature of the projects and assets that the issuer wants to finance/refinance and are generally aligned with such taxonomies as the Green Bond Principles or the Climate Bonds Taxonomy. The former describes broad categories of “green,” such as energy efficiency, renewable energy, sewage management systems, and air pollution, whereas the latter tends to use more specific terms, such as solar energy, low-carbon buildings (residential/commercial), and offshore wind and water.

Selection of projects and assets

This section in the document describes the issuer’s internal governance mechanism for selecting projects and assets. For instance, most issuers set up a selection committee consisting of senior staff from relevant departments (such as finance, engineering, and corporate social responsibility [CSR]), which will screen the underlying projects and assets according to the criteria disclosed in the use-of-proceeds section. This committee will recommend projects and assets to the board of directors for final approval.

A sovereign issuer would similarly describe its governance process. Relevant projects and assets could be screened by a joint committee comprising representatives of its finance and environment ministries (or their equivalent) and then sent to the legislature for final approval, if required.

Although each issuer might have a different way of selecting underlying projects and assets, it is critical that this selection process be as transparent as possible in order to provide investors with comfort that the issuer has robust internal processes.

Step 2. External Review

External review refers to independent assessment by an external auditor (reviewer) of the green credentials of a bond. Such external reviews fall under one of the following two categories.

Second-party opinions.

These are independent, research-based assessments on the likely climate performance of a green bond’s projects and assets. The methodology is generally designed by the opinion provider. Second-party opinions are issued at the pre-issuance stage and can vary quite a lot depending on the methodology used by the opinion provider.

Assurance.

This is an independent third-party audit undertaken in accordance with standards set by an independent standard setter (such as the Climate Bonds Initiative) that the auditor uses to assess a bond’s eligibility. Assurance opinions provide an assessment of the green credentials of the bond against both the standard and the internal procedures established by the issuer.

External reviewers are engaged while or soon after the issuer has set up a green bond framework, and their reviews are made public before the road show, to help promote the bond’s green credentials during the road show. It is now common practice for the independent review to accompany a bond’s prospectus when it is sent to potential investors.

Step 3. Post-Issuance Audit

To provide an extra layer of comfort to investors, issuers might decide to re-engage an external reviewer at the post-issuance stage. This kind of audit can refer to one of the following.

Post-issuance reviews.

The reviewer undertakes an assessment to provide investors with extra assurance that the proceeds are being allocated correctly to the nominated projects and assets. Although this step is voluntary in the second-party opinion model, it is mandatory under the Climate Bonds Standard and Certification Scheme.

Report audit.

The issuer might decide to engage a reviewer in order to assess its investor reports periodically (usually on an annual basis). The practice allows issuers to provide investors with the confidence that the key performance indicators are being met.

Policy Support by Various Governments and Regulators across the Globe

One key explanation for the increasing volume of green bonds is many states’ commitment to the 2015 Paris climate agreement. It is widely believed that countries are keen to showcase green initiatives to show their support for this UN-backed initiative. Signatories have agreed to actively combat global warming, notably by “pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels.” Major signatories include the European Union, China, India, and the United States (the latter three account for 42% of global greenhouse gas emissions). Although the Trump administration had announced that the United States would pull out from the agreement, President Joseph Biden has announced its re-entry.

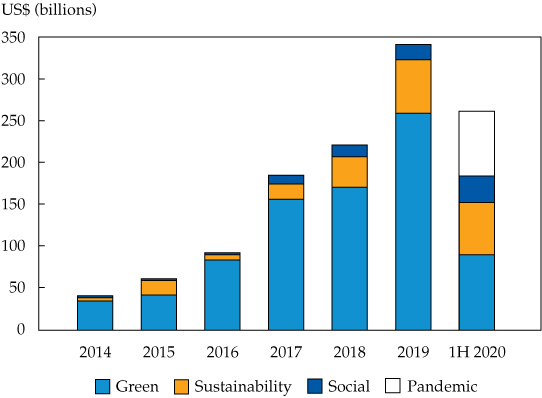

As a result of the global efforts at financing green assets, many countries have taken steps to encourage green bond issuances, and regulations are now in place in many countries, including China, which is also the only regulated green bond market in the world. Its Green Finance Committee has set out a detailed definition of processes and eligibility of projects. Other countries are also developing various types of green bond guidelines; these are already in place in Brazil, India, Japan, and Morocco. This kind of policy support has been one of the reasons why the volume of issuances has grown globally, as shown in Figure 1.

Figure 1. Green Bond Issuances, 2014–1H 2020

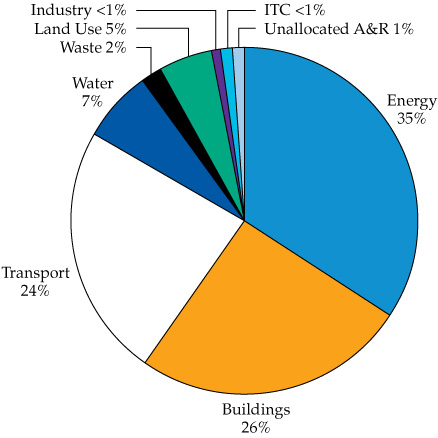

Green bonds have grown since 2014, as evidenced from Figure 1, and the use of proceeds has been dominated by buildings, energy, and transport, as shown in Figure 2. This predominance is partly explained by the facts that some of these sectors have traditionally represented a large proportion of the traditional financial system (buildings) and that some have seen tremendous growth resulting from policy thrusts and increasing financial attractiveness of the sector, especially renewable energy.

Figure 2. Use of Proceeds of Green Bonds, 1H 2020

Note: Unallocated A&R = Unallocated adaptation & resilience. ITC = Information technology and communications.

Although there have been many notable issuers, including multilateral development banks, such as EBRD, the World Bank, and International Finance Corporation, there have been many sovereign issuances, with 20-odd sovereign green issuances happening by the end of 2020.

One Example of an Issuer That Has Tapped the Market Repeatedly

ReNew Power Ltd. is India’s largest renewable energy independent power producer (IPP). As of early 2019, it had more than 7 gigawatts (GW) of commissioned and planned wind and solar generation facilities. The company is committed to leading a change in India’s current energy portfolio by delivering cleaner and smarter energy choices, thereby reducing the country’s carbon footprint. ReNew Power aims to play a pivotal role in meeting India’s growing energy needs in an efficient, sustainable, and socially responsible manner through innovation in solar and wind power solutions.

In March 2021, the company listed on NASDAQ through a SPAC (special purpose acquisition company) with a valuation of USD8 billion. A SPAC is a shell company set up by investors to raise capital through an IPO. SPACs are listed on a stock exchange to acquire another private company and take it public without the traditional IPO hassles.

After listing, ReNew Power announced that it plans to build a pipeline of around 18 GW to 19 GW of renewable capacity by the end of the fiscal year (FY) 2025.

ReNew Power has issued several green bonds, as detailed in Table 2.

Table 2. Green Bond Issuances by Renew Power over Time

|

Date of Issue |

Type of Instrument |

Size |

Country of Issue |

Climate Bonds Initiative Sector Criteria |

|

August 2016 |

Use-of-proceeds bond |

INR5bn (USD75m) |

India |

Wind |

|

February 2017 |

Use-of-proceeds bond |

USD475m |

Mauritius |

Solar and wind |

|

March 2019 |

Use-of-proceeds bond |

USD525m* |

India |

Solar and wind |

|

September 2019 |

Use-of-proceeds bond |

USD300m |

India |

Solar and wind |

|

January 2020 |

Use-of-proceeds bond |

USD450m |

India |

Solar and wind |

|

October 2020 |

Offshore bond, via India Green Energy Holdings |

USD325m |

India |

Solar and wind |

*Tapped twice: USD60m in March 2019 and USD90m in September 2019.

Conclusion

Since the time when green bonds began gaining traction, they have been subject to both cultist adulation and spiteful scorn. Some even suggest green bonds are ineffective because they lack “additionality”—that is, because bonds are primarily refinancing instruments and a bond issuance often does not finance a new project.

Green bonds are one instrument that helps achieve the goal of a low-carbon world, not a silver bullet for ensuring sustainability. Not all green bond issuers are necessarily low-emission companies, but hopefully they signal their desire to meet that goal through using such instruments.